UK Chancellor reveals Britcoin’s Roadmap: Savings not allowed!

On Monday, the UK Chancellor of the Exchequer, Jeremy Hunt, revealed that users wouldn’t be able to hoard their future CBDCs. Is the Chancellor confirming CBDC-critics’ concerns? Let’s find out.

Savings disabled?

In April 2021, the Bank of England and HM Treasury officially announced the launch of a central bank digital currency (CBDC) task force. Back then, the UK’s central bank said that their digital currency would co-exist “alongside cash and bank deposits, rather than replacing them.”

This week, the BoE Governor Andrew Bailey and Chancellor Jeremy Hunt revealed a CBDC roadmap which more or less aligns with the original statement. The UK’s Chancellor of the Exchequer is equivalent to the US’ Treasury Secretary (Janet Yellen).

He outlined the following points regarding the digital pound:

- It will probably be implemented in the second half of the decade by 2030.

- Holdings will be limited to a few thousand tokens to prevent unsustainable outflows from traditional high street banks.

The Chancellor is concerned that a shift to the digital pound would allow users to transfer money between accounts instantaneously. This would risk a bank-run event that could lead to the total collapse of the banking sector. As such, a limit on people’s digital pound holdings should be used, only until the introductory CBDC stage passes, they say.

“This would strike a balance between both encouraging use and managing risks, such as the potential for large and rapid outflows from banking deposits into digital pounds. These limits could be amended in the future” – Jeremy Hunt, UK’s Chancellor of the Exchequer

Similar to the United States, the UK’s banking sector is comprised of a handful of big banks – an oligopoly of sorts known as the ‘Big Four’: Lloyds Banking Group, Barclays, HSBC, and the Royal Bank of Scotland. Together, the four handle the majority of the United Kingdom’s financials, whether it’s credit cards, personal loans and finances as well as savings accounts and mortgages.

By design, CBDC tokens are built on different financial rails, and could essentially leave these legacy banks outside of the monetary loop. As such, artificial restrictions must be erected.

What Would a ‘Britcoin’ Look Like?

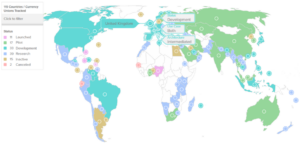

Presently, 11 countries have launched CBDCs. China, India, Russia, Australia and South Africa are in their piloting stage. Meanwhile, countries like the UK, North America and Europe are in the developmental stage, consisting of 33 nations. Notably, these tokens are guaranteed to be a step backwards for ordinary people who could have their money frozen or expire at a moment’s notice. In fact, the unspoken truth about CBDCs is that they are basically coupon codes, which explains central bankers’ eagerness to pursue them.

The current status of worldwide CBDC deployment. Image credit: Atlantic Council

This brings us to the first stumbling block regarding the nature of Central Bank Digital Currencies – will it be a central bank account or a token (like USDT or USDC)? In a tokenised format, a CBDC would represent a national currency issued and distributed by the central bank’s ledger. In this case, a tokenised CBDC could have built-in parameters such as limited privacy, which are sure to change depending on the financial environment or situational expedience.

In an account-based format, the CBDC would be under full control of the central bank. This would be similar to BUSD and Binance smart-chain situation, which is entirely controlled by Binance. Conversely, financial institutions would have an account with the central bank, in which transactions are credited and debited.

In the United States these developments are already underway. In fact, the Biden administration is developing a FedNow, a supposed upgrade to the Fedwire service. Unlike the previous updates, the FedNow platform would allow constant real-time settlements, in much the same way that Tether’s USDT functions on various networks (Ethereum, Tron, etc.). However, only banks would be able to clear real-time payments, who would in turn service retail users.

Similarly, the Bank of England is not exploring the option where retail users have a direct account with the central bank. Instead, the digital pound would be held in wallets which equate to physical banknotes. This is much like the Chinese eCNY. With a digital ID integrated on a smartphone, this would allow users to be fully integrated into the central bank’s digital pound without having a bank account. The European Union outlined its standard for eID as the universal digital wallet, which holds both government documents and tomorrow’s so-called digital euro.

For now, Chancellor Hunt is exploring “what is possible first, whilst always making sure we protect financial stability”.

What is the Difference Between Electronic Cash and CBDCs?

In practice, there is no obvious difference for users. It’s still an IoU controlled by a centralised cabal of people in suits who think they know better than you. In finance-speak, there is a difference in that dollar or pounds in mobile applications are claims on currency instead of actual currency.

This is the difference between a physical banknote and electronic cash. Like banknotes, the Federal Reserve and BoE have exclusive privilege to issue dollars or pounds, not commercial banks.

In other words, the Fed issues digital dollars, but they exist as the central bank’s reserve balance. In turn, commercial banks are given access to the Fed’s balance sheet which is not available to retail users. Jerome Powell, the Fed Chairman, once explained that the central bank could print money digitally at any moment, in addition to printing money physically.

In precisely the same manner, when the Bank of England purchased £895 billion worth of bonds (government debt) on January 5th, it printed banknotes digitally.

When you put it all together, it quickly becomes apparent that the entire point of CBDCs is not to facilitate payments, nor is it a breakthrough in monetary technology. The point is for central banks to gain direct access to retail users as the global sovereign debt crisis reaches its natural end-point. CBDCs function as a method of disintermediating commercial banks.

Since they’re programmable and not decentralised like Bitcoin or Litecoin, they can also be set to have an expiry date, or to have a coupon-like use-case. Incidentally, this is why the BoE and HM Treasury are talking about limiting savings and digital pound transfers. That’s just the tip of the iceberg in terms of what they’ll be able to do.

Whether that constitutes sound money is up to you, the reader. But in any case, the more fiat money rails and systems banks create, the more money will have to be printed. Retail users will pay off the difference through inflation, which is a roundabout way of taxing users.

Will the trade-off be worth it? The long and short of it is no, it won’t be.